The 50/30/20 Budget

The 50/30/20 Budget Rule: A Simple Guide to Financial Freedom

What is the 50/30/20 Budget Rule?

The 50/30/20 rule, popularized by Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, is a straightforward budgeting strategy that divides your income into three categories:

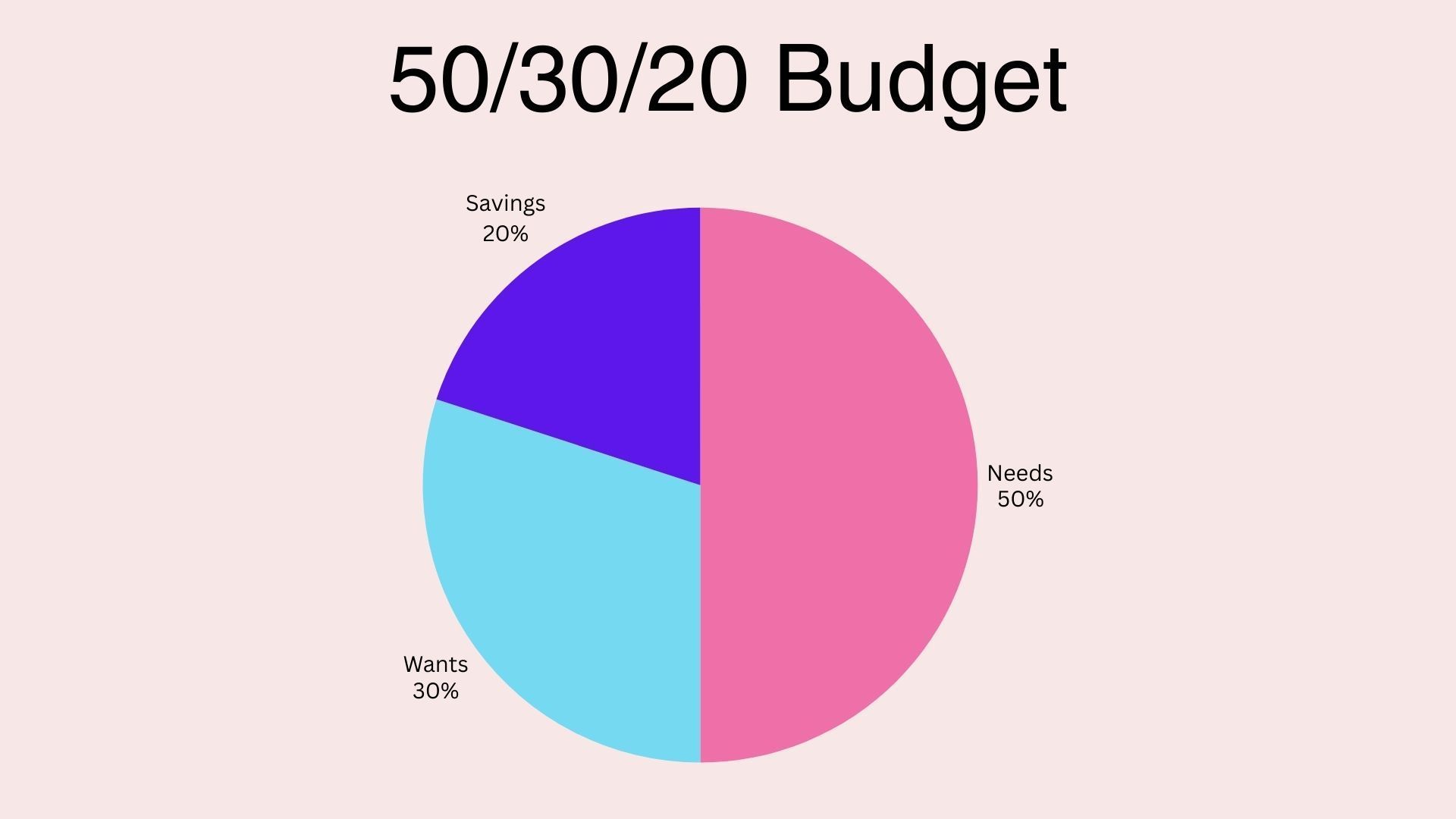

- 50% for Needs (essential expenses)

- 30% for Wants (discretionary spending)

- 20% for Savings (financial goals and debt repayment)

This structure helps you balance your financial responsibilities while ensuring you still have room for fun and future growth.

50%: Covering Your Needs

The largest portion of your budget—50% of your after-tax income—should go toward essential expenses. These are the non-negotiable costs necessary to maintain a basic standard of living.

What Counts as a "Need"?

Needs include:

- Housing: Rent, mortgage payments, property taxes

- Utilities: Electricity, water, gas, internet

- Groceries: Basic food and household supplies

- Transportation: Car payments, insurance, gas, public transit

- Insurance: Health, auto, life, and renter’s/homeowner’s insurance

- Minimum Debt Payments: If you have remaining debt, the minimum payments fall under this category

If you find that your essentials exceed 50% of your income, it may be time to reevaluate and cut costs where possible—such as downsizing housing or switching to a cheaper phone plan.

30%: Enjoying Your Wants

The next 30% of your income is for wants, which are non-essential but enjoyable expenses that improve your quality of life.

What Counts as a "Want"?

Wants include:

- Dining Out: Restaurants, coffee shops, fast food

- Entertainment: Movies, concerts, video streaming subscriptions

- Shopping: Clothes, gadgets, home decor

- Travel: Vacations, weekend getaways

- Hobbies & Activities: Gym memberships, books, gaming

While these expenses are not critical for survival, they contribute to personal happiness and well-being. The key is to enjoy them responsibly without overspending.

How to Keep Wants in Check

If your wants exceed 30% of your budget, consider:

- Limiting the number of streaming services you subscribe to

- Cooking at home more often

- Finding free or low-cost hobbies

By maintaining this balance, you can still enjoy life while staying financially responsible.

20%: Building Your Future with Savings

The final 20% of your income goes toward savings and financial goals. This is the category that will help you build wealth, prepare for emergencies, and secure your future.

What Counts as "Savings"?

Savings should be allocated toward:

- Emergency Fund: A safety net for unexpected expenses (aim for 3-6 months of expenses)

- Retirement Savings: Contributions to a 401(k), IRA, or other investment accounts

- Debt Repayment: Paying extra toward high-interest debt to become debt-free faster

- Investments: Stocks, bonds, real estate, or other wealth-building assets

Prioritizing Savings

If you’re just starting out, focus on building an emergency fund first, then contribute to retirement and additional savings goals. If you’re debt-free, you can maximize this category by investing in long-term financial growth.

Implementing the 50/30/20 Budget

Now that you understand the breakdown, here’s how to apply it to your finances:

- Calculate your after-tax income – If your salary is $4,000 per month after taxes:

- Needs: $2,000 (50%)

- Wants: $1,200 (30%)

- Savings: $800 (20%)

- Track your spending – Use budgeting apps like Mint, YNAB, or spreadsheets.

- Adjust as needed – If one category is too high, find areas to cut back.

This simple system makes budgeting easier and keeps your spending intentional.

Get a Personalized Debt Plan with Sally

If you’re looking for a personalized approach to budgeting or need help managing your debt, Sally can guide you through a custom debt repayment plan. Whether you’re working on an emergency fund, tackling student loans, or planning for retirement, a strategy tailored to your unique situation can make all the difference.

Ready to take control of your finances?

Contact Sally Bernard